Brief: Liquity

Brief: Liquity

A low cost and efficient borrowing service

Credits: The Shrimp (previously obeseolaf)

Introduction

Liquity is a decentralized borrowing protocol that allows users to draw interest-free loans against ETH which is used as collateral. Loans are paid out in LUSD (a USD pegged stablecoin) where users need to maintain a minimum collateral ratio (MCR) of 110%.

Key Features

There is 0% interest rate for borrowers, as such there is no risk or fear of accruing debt. Fees are only charged when borrowing LUSD and redeeming ETH [ redeeming ETH and repaying debt are different, but more on that later ]

Censorship resistance - unlike most other protocols, Liquity does not operate their own Frontend application, instead relying on a network of independent Frontend Operators which helps to bootstrap a decentralized ecosystem of actors.

Borrowing

To borrow a user must open a Trove and deposit a certain amount of collateral (ETH). The user can then draw LUSD from a MCR of 110%. A minimum debt of 2,000 LUSD is also required. Furthermore, the protocol does not provide opportunities for users to lend tokens.

What is a Trove?

A Trove is where you take out and maintain your loan. Each Trove is linked to an Ethereum address and each address can have just one Trove. If you are familiar with Vaults from other platforms, Troves are similar in concept.

When making a deposit into a Trove, two other ‘fees’ also taken into account which are the Borrowing Fee and the Liquidation Reserve.

The Borrowing Fee is added to the debt of the Trove and is given by the baseRate which is confined to a range between 0.5% and 5%, multiplied by the amount of liquidity drawn by the user. [ see Soft Peg Mechanisms to understand how the baseRate changes ]

When you open a Trove and draw a loan, 200 LUSD is set aside as a way to compensate gas costs for the transaction sender in the event your Trove is liquidated. The Liquidation Reserve is fully refundable if your Trove is not liquidated, and is given back to you when you close your Trove by repaying your debt. The Liquidation Reserve counts as debt and is taken into account in the calculation of a Trove's collateral ratio, slightly increasing the actual collateral requirements.

Troves maintain two balances: one for ETH acting as collateral and the other for debt denominated in LUSD. You can change the amount of each by adding collateral or repaying debt. As a user makes changes to his balance, the Trove’s collateral ratio changes accordingly.

Sam opens a Trove and deposits 2 ETH at a price of 2000 USD (4000 USD in total as collateral). Sam wants to borrow 2,000 LUSD and the Borrowing Fee charged would depend on the baseRate which now stands at 2.5%. After the Liquidation Reserve (200 LUSD) and Borrowing Fee (50 LUSD) are added, Sam incurs a debt of 2,250 LUSD. This gives Sam a Collateral Ratio (CR) of 177% (CR = 100% * 4000/2250). Sam now wishes to repay some of his debt, and deposits 250 LUSD into his Trove. Sam’s CR is now 200% (CR = 100% * 4000/2000, assuming the price of ETH remains at 2000 USD)

Minimum Collateral Ratio (MCR) and Liquidation risk

The MCR is the lowest ratio of debt to collateral that will not trigger a liquidation under normal operations. This is a protocol parameter that is set to 110%. So if your Trove has a debt 10,000 LUSD, you would need at least $11,000 worth of ETH posted as collateral to avoid being liquidated. To avoid liquidation during Recovery Mode, it is recommended for a user to keep the ratio comfortably above 150%. [ see Recovery Mode to find out more ]

The underlying collateral (ETH) is lost as the LUSD debt is paid off through liquidation. As such, a user will no longer be able to retrieve their collateral by repaying debt. A liquidation at a MCR of 110% thus results in a net loss of 9.09% (100% * 10 / 110) of the collateral’s Dollar value.

LUSD and Redemptions

In recent months there has been a lot concern regarding the health of DeFi protocols and stablecoins in particular [ read up more about Tron’s new stablecoin USDD and the collapse of UST ]. As such, it is important to understand how LUSD maintains its peg which is achieved through “Hard Peg Mechanisms” and “Soft Peg Mechanisms”.

Hard Peg Mechanisms

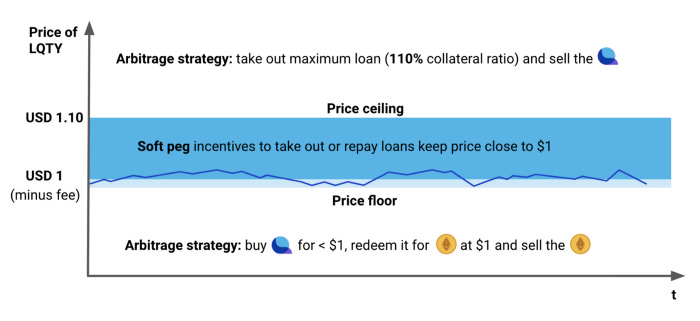

One of the core innovations of Liquity is that LUSD is redeemable against the underlying collateral held by the borrowers. That means, every LUSD holder can exchange their coins for ETH at face value, i.e. for every 1 LUSD they would get 1 USD worth of ETH. When LUSD is redeemed, the ETH provided to the redeemer is allocated from the Trove(s) with the lowest collateral ratio (even if it is above 110%). If at the time of redemption you have the Trove with the lowest ratio, you will give up some of your collateral, but your debt will be reduced accordingly. You can think of redemptions as if somebody else is repaying your debt and retrieving an equivalent amount of your collateral. As a positive side effect, redemptions improve the collateral ratio of the affected Troves, making them less risky. [ to learn more about redemptions click here ]

An important feature of redemptions is that they help protect LUSD’s price floor of $1 through direct arbitrage. When LUSD is floating below peg, an arbitrageur can simply redeem their LUSD against the system as if it was worth $1 and immediately sell the redeemed ETH at a higher price. Since the redeemed LUSD is burned by the protocol, the stablecoin supply (monetary base) will shrink upon every redemption, which has a positive effect on the price.

Further more, the MCR of 110% creates a natural price ceiling at USD 1.10. When the LUSD:USD exchange rate exceeds that level, borrowers can make an instant profit by borrowing the maximum amount against their collateral and selling the LUSD on the market for more than USD 1.10. If 1 LUSD trades at USD 1.11 for example, you can lock up USD 110 worth of ETH, take out a loan of 100 LUSD and sell it for USD 111. No matter if your loans gets liquidated or not, you have made an arbitrage gain of 1 USD. It is expected that the arbitrage opportunity will steer LUSD away from reaching USD 1.10 and if it ever hits the ceiling, it will rebound very quickly. This should mitigate a mass influx of risky loans taken out at the minimum collateral ratio in such breakout situations.

A summary of Hard Peg Mechanisms can be seen below:

Soft Peg Mechanisms

To enhance user experience for low-collateral borrowers whose loans (Troves) may be vulnerable to redemptions, the system charges a one-off fee on every redemption, called the Redemption Fee. Both the Redemption Fee and Borrowing Fee are affected by the baseRate. When redemptions occur more frequently (which signals that LUSD is likely worth less than the USD), the system’s baseRate increases, in turn causing Liquity’s one time Borrowing Fee to increase — discouraging people from borrowing and dampening the amount new LUSD entering the market. When redemptions aren’t occurring, the baseRate gradually decays over time, making it cheaper to borrow and encouraging new LUSD to enter the market. Thus, the Borrowing Fee and the Redemption Mechanism work in tandem to slow down / ramp up growth of the monetary base if needed

Stability Pool

One major concern for borrowing services is that the protocol must remain solvent. In order to achieve this, protocols need to have a reserve of funds (stablecoins) that they use to manage liquidations.

In Liquity, The Stability Pool acts as source of liquidity that repays debt from liquidated Troves. This ensures that the total LUSD supply always remains backed which helps to serve both system stability (solvency) and price stability.

When any Trove is liquidated, an amount of LUSD corresponding to the remaining debt of the Trove is burned from the Stability Pool’s balance to repay its debt. In exchange, the entire collateral from the Trove is transferred to the Stability Pool.

The Stability Pool is funded by users transferring LUSD into it (called Stability Providers). Over time Stability Providers lose a pro-rata share of their LUSD deposits, while gaining a pro-rata share of the liquidated collateral (ETH). However, since Troves are likely to be liquidated at just below a 110% collateral ratio, it is expected that Stability Providers will receive a greater dollar-value of collateral relative to the debt they pay off. However this also increases the Stability Providers exposure to ETH, which puts them at risk if the price of ETH crashes.

How can a stability provider gain from liquidations?

Stability Providers will most likely experience a net gain whenever a Trove is liquidated, allowing them to have an attractive return option on their deposited LUSD.

Let’s say there is a total of 10,000 LUSD in the Stability Pool and Sam’s deposit is 1,000 LUSD. Now, a Trove belonging to Ashley with debt of 2,000 LUSD and collateral of 4 ETH is liquidated at an ETH price of $545, and thus at a CR of 109% (CR = 100% * (4 * 545) / 2,000). When Ashley’s Trove is liquidated, 2,000 LUSD (her debt) is burned from the Stability Pool and 4 ETH is transferred to the Pool itself. Given that Sam’s pool share is 10%, his deposit will go down by 10% of the liquidated debt (200 LUSD), i.e. from 1,000 to 800 LUSD. In return, he will gain 10% of the liquidated collateral, i.e. 0.4 ETH out of 4 ETH, which is currently worth $218. Your net gain from the liquidation is $18.

Furthermore, after making his/her first deposit, a user will start accumulating a reward (LQTY) proportional to the size of his deposit on a continuous basis. The reward is calculated according to the rewards schedule and the kickback rate of the Frontend that he used for making the deposit. Rewards will be the highest for early adopters of the system.

Recovery Mode

Recovery Mode kicks in when the Total Collateral Ratio (TCR) of the system falls below 150%. TCR is the ratio of the Dollar value of the entire system collateral at the current ETH:USD price, to the entire system debt. In other words, it is the sum of the collateral of all Troves expressed in USD, divided by the debt of all Troves expressed in LUSD. During Recovery Mode, Troves with a CR below 150% can be liquidated.

Moreover, the system blocks borrower transactions that would further decrease the TCR. New LUSD may only be issued by adjusting existing Troves in a way that improves their collateral ratio, or by opening a new Trove with a collateral ratio more than or equal 150%. In general, if an existing Trove's adjustment reduces its CR, the transaction is only executed if the resulting TCR is above 150%.

Economically, Recovery Mode is designed to encourage collateral top-ups and debt repayments. It also acts as a self-negating deterrent: the possibility of it occurring actually guides the system away from ever reaching it. Recovery Mode is not a desirable state for the system.

During Recovery Mode it is also important to note that Redemption Fees are still affected by the baseRate while the Borrowing Fee is set to 0% to encourage borrowing to raise the TCR.

LQTY Staking

LQTY is the secondary token issued by the Liquity protocol. It captures the fee revenue that is generated by the system and incentivizes early adopters and Frontend Operators.

LQTY rewards will only accrue to Stability Providers, i.e. users who deposit LUSD to the Stability Pool, and Frontend Operators who facilitate those deposits. LQTY is also not a governance token.

Why should I stake LQTY?

Users can deposit the LQTY token to the Liquity staking contract. Once done a user will start earning a pro rata share of the Borrowing Fees and Redemption Fees in LUSD and ETH.

Current Market Conditions and Risks

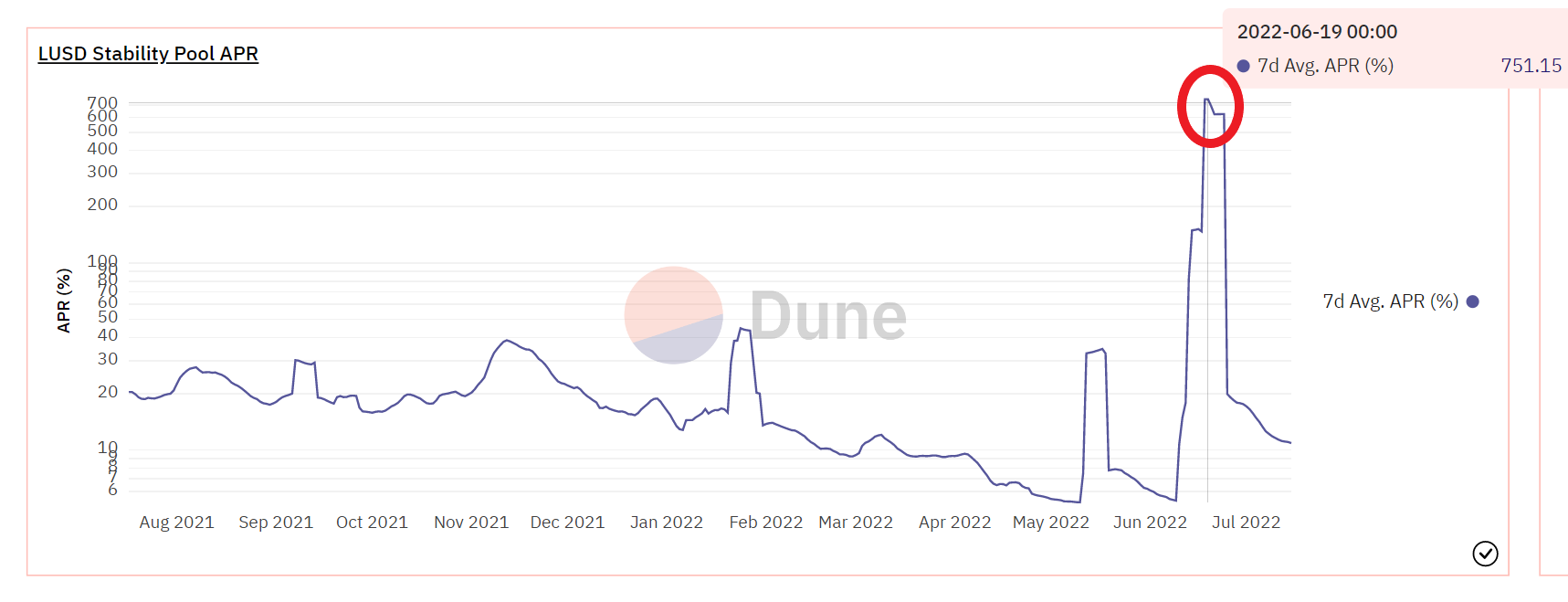

With the crypto markets down and the price of ETH dropping sharply in June, Liquity saw many liquidation events. Among them was the biggest event so far which took place on the 18th of June involving a Trove with close to 61 million LUSD in debt.

Liquity’s stability pool depositors received 71.5k ETH from this single transaction, and it also meant that the APR for the week of June 13th for Stability Pool providers rose to 751%, an all time high. [ click here to see the transaction on Etherscan ]

A snapshot of the Liquidation event and APR spike can be seen below:

In addition, with rise in liquidation events, more users have repaid their debts and effectively closed their Troves. As such, the number of Troves has decreased drastically from around 1000 in May to only 500 in June as seen below:

In spite of the market volatility, the price of LUSD has remained relatively stable due in part to their Hard Peg and Soft Peg Mechanisms. A snapshot of the price chart can be seen below:

Conclusion

All in all, Liquity is a solid borrowing service. It is more competitive compared to protocols which use a pooling model like Aave or Compound as the user is able to borrow directly from the protocol at a lower cost without relying on deposits from others. It is also able to offer more predictable fees (Borrowing Fees and Redemption Fees) where the rate is fixed and clearly stated at the time of the loan as opposed to MakerDao which practices a variable annual rate.

Although not elaborated on in this article, while in normal mode, it is one of the most permissive borrowing services in terms of leverage. It is possible for a user to achieve a maximum leverage ratio of 11 times, where the user sells borrowed LUSD on the market for ETH and uses the latter to top up the collateral of his / her Trove. This allows the users to draw and sell more LUSD, and by repeating the process reach the desired leverage ratio. Of course, I would not recommend this strategy given that the risk of liquidation is extremely high. [ click here for more information on leverage ]

The team behind Liquity is also working hard to bring LUSD onto layer 2s, recently announcing that Celer’s Cbridge now supports bridging of LUSD between Optimism and Ethereum. The Liquity treasury has also been whitelisted on Curve with the aim of of boosting participation in the governance of Liquity.

Even though it remains a lesser known protocol, Liquity as a service has proven to be resilient and has shown that it is able to weather times of great market uncertainty.